Buying a Fixer-Upper in Albuquerque in 2026: How 203k and HomeStyle Renovation Loans Work and Which Neighborhoods Have the Best Value-Add Inventory

There is something about driving down a block in the South Valley or cutting through the older streets near Old Town and spotting a house with good bones, a sagging porch, and a yard full of potential that makes a certain kind of buyer slow down and think. If that is you, you are not alone. The fixer-upper Albuquerque 2026 market is drawing serious attention from first-time buyers, investors, and longtime locals who are tired of being outbid on move-in-ready homes and ready to roll up their sleeves instead.

The good news is that the financing tools to make this work have gotten more accessible, and the neighborhoods with real upside are still findable if you know where to look. This is not a theoretical conversation. This is what we are seeing on the ground right now, and what buyers we work with are actually doing to get into homes they can build equity in from day one.

How FHA 203k Loans Work for Albuquerque Home Buyers

The FHA 203k loan is one of the most underused tools in the Albuquerque home buyer's toolkit. It is a single mortgage that wraps both the purchase price of the home and the estimated cost of renovations into one loan, backed by the Federal Housing Administration. You close once, you get one monthly payment, and the renovation funds are held in escrow and released as work is completed.

There are two versions worth knowing:

- •Limited 203k (sometimes called the Streamline): Covers non-structural repairs up to $35,000. Think new flooring, kitchen updates, roof repairs, HVAC replacement, fresh paint, and bathroom remodels. This is the path most first-time buyers in ABQ take.

- •Standard 203k: Covers major structural work, additions, full gut renovations, and projects over $35,000. It requires a HUD-approved consultant to oversee the process, which adds a layer of complexity but also opens the door to properties that need serious work.

For a 203k loan Albuquerque New Mexico buyers need to meet standard FHA credit and income guidelines, which generally means a credit score of 580 or above with 3.5 percent down. The property has to be your primary residence, which rules it out for pure investment flips, but it is perfect for the buyer who wants to live in the home while building sweat equity.

One thing that trips people up locally: not every lender in Albuquerque actively offers 203k loans. Some banks technically have the product but have not processed one in years and do not have the internal workflow to handle the escrow draws and contractor coordination. When you are shopping lenders, ask specifically how many 203k loans they have closed in the last twelve months. You want someone who does these regularly, not someone learning on your deal.

How the Fannie Mae HomeStyle Renovation Loan Compares

The HomeStyle renovation loan is the conventional counterpart to the 203k, backed by Fannie Mae rather than the FHA. If you have stronger credit and a larger down payment, this product often makes more sense.

Here is how it stacks up differently:

- •No mortgage insurance with 20 percent down: Unlike FHA loans, which carry mortgage insurance for the life of the loan in most cases, HomeStyle lets you eliminate PMI once you hit 20 percent equity.

- •Higher loan limits: Conventional conforming limits in Bernalillo County are higher than FHA limits, which matters if you are buying in a neighborhood where even the fixer-uppers are not cheap.

- •Investment properties allowed: HomeStyle can be used on second homes and investment properties, not just primary residences. This makes it a legitimate tool for the Albuquerque landlord or house hacker.

- •Renovation budget up to 75 percent of the as-completed appraised value: This gives you serious room to work with on a major renovation.

The tradeoff is that HomeStyle typically requires a higher credit score, usually 620 or above, and the underwriting process can feel more rigorous. But for the buyer who qualifies, it is a cleaner product in many scenarios.

“The renovation loan conversation in Albuquerque has shifted. Buyers who would have passed on a home needing $40,000 in work two years ago are now running the numbers differently, because the math on a value-add purchase often beats competing for a turnkey home in the same zip code.

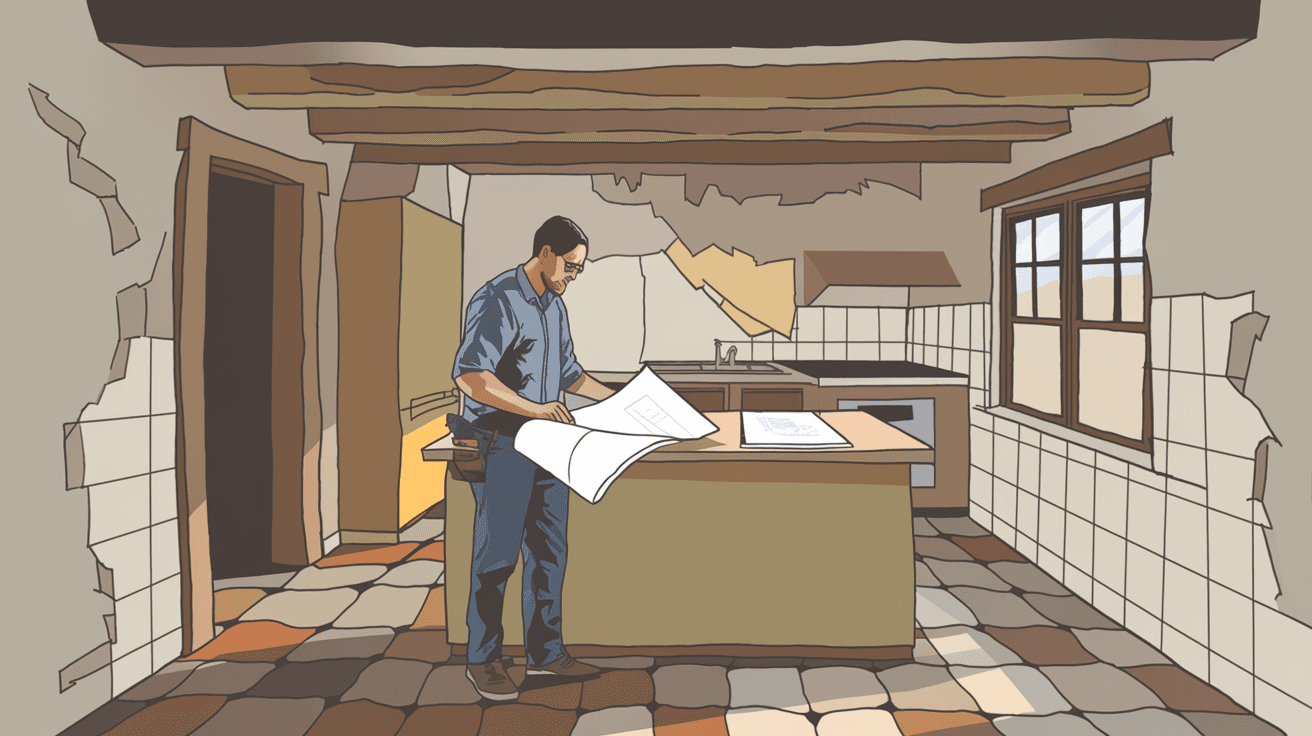

The Renovation Loan Process Step by Step

Understanding the mechanics of a renovation loan Albuquerque home buyer process will save you a lot of stress. Here is what the timeline actually looks like:

- •Get pre-approved first: Your lender will underwrite you based on your income, credit, and the projected after-renovation value of the home. You need this number before you start making offers.

- •Find the property and get it under contract: Your offer should include language noting the purchase is contingent on renovation financing approval.

- •Get contractor bids: For 203k loans, your contractor must be licensed and approved. For Standard 203k, a HUD consultant will also inspect and sign off on the scope of work. Albuquerque has a solid pool of licensed contractors familiar with this process, but get multiple bids.

- •Appraisal based on as-completed value: The appraiser reviews your renovation plans and assigns a value to what the home will be worth after work is done. This number drives how much you can borrow.

- •Close on the loan: Renovation funds go into escrow. You own the home.

- •Renovation begins: Work happens in stages, with draws released from escrow as each phase is completed and inspected.

- •Move in or continue living there: For many buyers, you can occupy the home during renovation depending on the scope of work.

The full process from offer to close typically runs 45 to 60 days on a well-run 203k deal. Budget for that timeline when you are negotiating.

Fixer-Upper Albuquerque 2026: Which Neighborhoods Have the Best Inventory

Not every part of the city offers the same opportunity. You want the intersection of three things: affordable acquisition prices, enough comparable sales to support a strong after-renovation appraisal, and a neighborhood trajectory that is moving in the right direction. Here is where we are seeing real opportunity heading into 2026.

South Valley: The Best Value-Add Neighborhood in ABQ Right Now

If there is one area where the fixer-upper Albuquerque 2026 conversation keeps coming back to, it is the South Valley. The median price sits around $265,000, which means you can often acquire a property with renovation potential without stretching your budget before you even swing a hammer.

The South Valley has deep roots. This is a community with generational families, working farms, horses on residential lots, and a cultural richness that does not exist anywhere else in the metro. The stretch along Isleta Boulevard, the side streets near the Rio Grande bosque, the older neighborhoods off Arenal Road, these are places where a well-renovated home stands out immediately and appraisals reflect the improvement.

The school district is APS, with various elementary schools feeding into Rio Grande High School, which has a strong community identity. For buyers with kids or planning for the future, that local connection matters.

The insider tip that only people who actually work this area know: properties that back up to the acequia system or have mature cottonwood trees on the lot appraise noticeably higher than comparable homes without those features. If you find a fixer-upper in the South Valley with water rights or bosque access, that is a serious asset that many buyers from outside the area do not recognize until it is pointed out to them.

Barelas and the Rail Yards Adjacent Streets

Barelas has been on the edge of a breakout for several years, and the renovation activity happening near the Rail Yards Market area is starting to show up in comp values. Original Craftsman bungalows and older territorial-style homes here are the kind of properties that respond beautifully to thoughtful renovation. The proximity to Downtown, the BioPark, and the Rio Grande Nature Center makes the after-renovation story easy to tell to an appraiser.

The International District

The International District along Central Avenue east of Louisiana gets unfairly dismissed by buyers who do not spend time there. The housing stock is older, the lots are generous, and the acquisition prices remain low relative to what a renovated home can appraise for. The cultural fabric of this neighborhood, the restaurants, the community organizations, the proximity to Nob Hill, is an asset that is increasingly recognized by younger buyers who want a real neighborhood, not a subdivision.

Wells Park and the North Valley Fringe

North of Downtown and west of the freeway, Wells Park and the streets connecting toward the North Valley offer older homes on larger lots at prices that still make renovation math work. The North Valley itself has gotten expensive, but the transitional streets on its southern edge still have inventory worth examining.

“In Albuquerque, the best fixer-upper deals are rarely on the main boulevards. They are on the quiet streets one block off the action, in neighborhoods where the trajectory is clear but the prices have not fully caught up yet.

What to Watch Out for in Albuquerque Fixer-Uppers Specifically

Buying a renovation project in ABQ comes with some local-specific considerations that a generic home buying checklist will not catch.

- •Adobe and vigas: Older adobe homes are beautiful and energy efficient, but deferred maintenance on an adobe structure can mean significant cost. Water intrusion into adobe walls is a serious repair. Always get a specialized inspection from someone who knows adobe construction, not just a standard home inspector.

- •Swamp cooler versus refrigerated air: Many older homes in Albuquerque still run evaporative coolers. Converting to refrigerated air is a popular renovation that adds value, but it requires electrical upgrades and proper ductwork. Build this into your renovation budget if the home does not already have it.

- •Lot drainage and caliche: Albuquerque's caliche soil layer creates drainage challenges that are not always visible during a dry season showing. Ask about monsoon season flooding history. The neighbors will tell you the truth if you ask them directly.

- •Acequia rights and water shares: In the South Valley and North Valley especially, water rights attached to a property have real monetary value. Confirm whether the property has active water shares before closing.

- •Lead paint and asbestos: Homes built before 1978 require lead paint disclosure. Many older ABQ homes also have asbestos in floor tiles or insulation. Factor testing and remediation into your renovation budget.

Working With a Real Estate Team That Knows This Process

The renovation loan process requires coordination between your real estate agent, your lender, your contractor, and the appraiser. When any one of those pieces is out of sync, deals fall apart or timelines blow up. Working with an agent who has walked through this specific process with buyers, who knows which streets in the South Valley are worth fighting for and which ones have title issues that will slow you down, makes a material difference in whether you close or not.

If you are seriously considering a fixer-upper purchase in Albuquerque and want to talk through what your renovation budget could realistically buy in today's market, reach out to The Taylor Team at Berkshire Hathaway HomeServices. We can run the numbers with you before you ever write an offer.

The fixer-upper path is not for everyone, but for the right buyer in the right neighborhood with the right financing in place, it remains one of the most reliable ways to build equity in Albuquerque's 2026 market. The bones are out there. You just have to know where to look.

Want more insider intel?

Subscribe to get market updates and new articles delivered to your inbox.